Where do Healthcare Budgets Match AI Hype? A 10-Year Lookback of Funding Data

Authors: Parth Desai and Jake Rubin

Introduction

It’s hard not to have a conversation in 2024 without some mention of artificial intelligence (AI). The technology is increasingly top-of-mind for America’s corporate leaders. Yet, for many, the concept is still abstract. We know AI has tremendous potential to transform how we go about our day-to-day activities, but we are still discovering where it will have the biggest impact. Perhaps this is why our collective concern is outweighing our excitement about the technology. It may also be why lofty enthusiasm about the technology is pulling back to match a new reality.

Nowhere is the dichotomy between potential value and an embrace of AI more apparent than the healthcare sector, where adoption is relatively early to meet enormous potential. So, in this analysis, we’ve reviewed over 4,000 healthcare AI venture capital deals across a decade to understand where AI companies have created the most value. We hope the insights gleaned help inform where to focus future AI efforts.

Table of Contents

1) Healthcare’s AI Opportunity: Will the Hype Endure?

5) Conclusion

6) Methodology and Disclaimers

Healthcare’s AI Opportunity: Will the Hype Endure?

Some estimates suggest AI could create $370 Billion in value for healthcare, one of the largest opportunities across any US sector. This makes sense, given healthcare’s notoriously low productivity relative to the US economy. It’s no wonder that budgetary allocations to AI are soaring. Investors, seeking to tap into these budgets, poured over $30 Billion of capital into healthcare AI¹ companies over just the last 3 years. This is amongst the largest sums across any sector. In fact, over a 3-year period, 47% of all healthcare venture capital deals were in companies leveraging AI. This is compared to an average of 28% in the decade prior to 2021².

Major technological advances have been a harbinger of frenzied investing efforts, with historical funding data highlighting that AI deal activity spiked in 2013 (advent of deep learning models) and then again in 2021–2022, on the heels of OpenAI’s generative AI advances.

Despite this, healthcare enterprises continue to be middling in AI adoption, with only about 6.8%³ of organizations reporting that they plan to leverage the technology in the next 6 months (compared to 21.5% of leading sectors). Tremendous potential has been tempered by warranted skepticism, as leaders seek to understand how to balance targeted use cases with risks and return on investment. 2022 and 2023 funding data sheds further light into this phenomenon, with a marked deceleration in healthcare AI funding compared to overall healthcare funding. Unsurprisingly, funding plateaus also followed funding spikes in the year after deep learning and transformer model advancements. AI hype cycles in healthcare seem to be followed by periods of sobering reality in which budgetary increases lag funding increases, and the industry learns where and how to best use the technology.

Interestingly, unlike previous technology hype cycles, healthcare budgetary allocations to AI broadly are now slightly higher than cross-sector averages, suggesting a potentially more enduring commitment to this technology. However, healthcare has typically been a more prudent buyer of emerging technology, carefully weighing financial benefits with impact on the patient and clinician experience of care. We therefore believe that healthcare buyers will initially allocate their growing budget to areas where they’ve observed durable return on investment in the past, before standing on unproven ground.

Below, we analyze funding data trends to highlight historically enduring areas for health systems and health plans in particular, and consider implications for future opportunity. In future articles, we will also explore life sciences AI funding data in more detail.

Insights from a Decade of Healthcare AI Funding: Life Sciences and Health Plans Convert Capital to Value More Efficiently

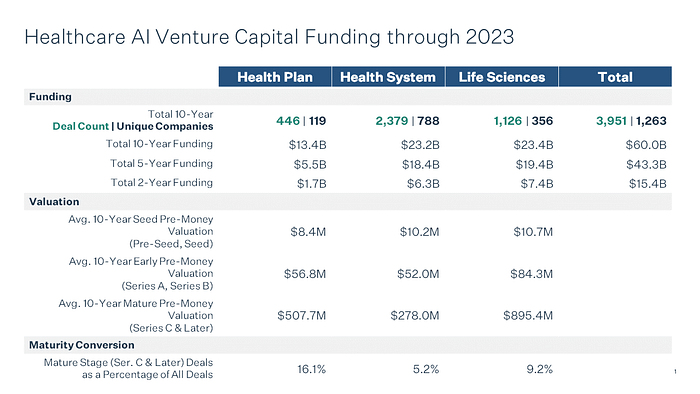

Healthcare AI startups selling into health systems, health plans and life sciences have raised around $60 Billion over the last decade, as highlighted in the table below. Interestingly, over 70% of this capital has been raised in the last 5 years, which makes sense, given the period coincided with meaningful advances in AI technology, more favorable capital market dynamics and new technology needs catalyzed by the pandemic. All of these dynamics fueled expanded information technology (IT) budgets and enthusiasm to invest into innovation.

More capital, however, does not universally equate to more value creation. Most AI startups in the health system segment, for example, have not matured beyond Seed and Early stages (Series A, Series B), a consistent trend over the last decade. While just over 5% of health system AI startups have reached a Mature stage (Series C or later) almost 10% of life sciences AI startups and roughly 16% of health plan AI startups reached an equivalent stage. Overall, this suggests that life sciences and health plan focused AI startups have been able to create more value for their customers and have been more enduring.

But there is likely more to this phenomenon. Health plan and especially life science enterprises typically have higher operating margins and an ability to commit a greater percentage of operating budget to IT and innovation, which means they often have more resources and patience to scale AI projects. As we will address in a follow up piece, R&D as a percentage of revenue for life sciences enterprises dwarfs most other sectors, meaning life science enterprises also have a higher willingness to invest in any technology that streamlines these currently inefficient processes. Some of this shows up in the venture funding data we analyzed, but there is likely also a substantial amount of budget devoted to internal development efforts and other privately funded AI companies that were not captured in this dataset.

This dynamic is further supported by the fact that the average valuations (often pegged to a multiple of revenue / revenue growth in the venture business) of Mature stage health plan and life sciences AI startups far exceed those of startups that have reached maturity in the health system segment. In fact, the step up in average valuation between Seed and Mature stage AI startups selling into life sciences is over 84x, which is 1.4x as large as health plan AI startups and almost 4x as large as health system AI startups. The valuation data in the table above seems to indicate that investors inordinately reward those life sciences AI startups that are able to scale.

Nonetheless, significant value has been created by AI startups targeting the health system and health plan enterprise. The magnitude of capital and value creation in these segments, however, has been concentrated amongst just a handful of functional areas.

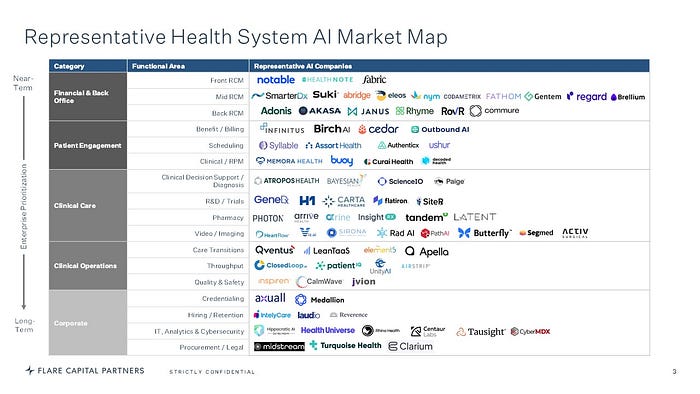

Health System AI Landscape: Clinical AI Solutions Grow into Their Massive Potential, While Financial and Operating Efficiency Continues to Reign Supreme

With labor comprising over 60% of revenue, health systems have a significant productivity imperative and no shortage of need for AI-driven efficiency. Unsurprisingly, more startups selling AI to health systems have been created over the last 10 years than any other healthcare segment that we analyzed. These startups have collectively raised over $23 Billion in capital, as shown below. While the clinical AI category has been the highest-funded category, we believe near-term AI budgets will prioritize financial, patient engagement and operational throughput value propositions that have historically yielded more tangible ROI.

Almost 50% of health system AI funding has gone towards clinical care AI startups enabling imaging, clinical decision support and diagnostic value propositions. This has been a consistent trend, when looking back at 10-, 5- and 2-year periods. The allure of leveraging AI to streamline and enhance clinical decision making accuracy as well as mitigate persistent labor challenges (shortages and costs) has driven this enthusiasm. Despite investor interest, clinical decision support solutions have yielded amongst the lowest maturity rates amongst all health system AI startups (6.8%) while imaging AI solutions have fared slightly better with a 9.9% maturity rate. Furthermore, startups addressing these functional areas have higher capital intensity rates relative to their average valuations and scaled value creation.

This likely speaks to the fact that clinical workflows directly impacting care decisions pose the highest risk and liability to care providers. Therefore, these solutions necessitate a higher threshold of accuracy, and their reliability and auditability are closely scrutinized and heavily regulated. This can lead to longer sales and implementation cycles. It can also be difficult to parse the value created by these solutions from decision-making by clinicians, who are ultimately liable for care outcomes. These dynamics can muddle return on investment attribution.

Importantly, reimbursement frameworks to support technology-led clinical interventions are also nascent, challenging business models in this segment. Notably, several of the more mature imaging AI startups have secured FDA clearance for their diagnostic algorithms, which has likely helped them mitigate the reimbursement challenges faced by their peers. Clearly, the time and capital required to productize and monetize clinical AI products, combined with more limited relative pricing power, has hampered an ability to scale as rapidly as products targeted to other value propositions.

Despite these challenges, there have been a handful of breakout clinical care AI products developed over the last several years. The most valuable and mature startups in this category today have developed care delivery models that leverage AI to anticipate clinical deterioration earlier than a human clinician. These insights can be used to develop advanced preventative care plans that are also more personalized, allowing care teams to coordinate care more efficiently and avoid unnecessary utilization. Importantly, these products also strike an important balance of preserving the clinical autonomy that clinicians deeply value. Combined, leading startups are showing that AI can yield valuable resource efficiency and superior clinical outcomes when thoughtfully wrapped into a new care model.

It is worth noting that clinical care AI startups supporting research and development and/or clinical trial functions within the health system enterprise have commanded some of the highest valuations in the clinical care AI category. This seems to reflect the fact that they can create value for and commercialize their health system partnerships as well as life sciences R&D partnerships, a meaningfully larger total addressable market opportunity.

For similar reasons, we also believe there is a unique and emerging role for AI to play in improving pharmacy operations. Though the functional area has not been as well funded as other clinical areas, pharmaceutical costs are soaring and creating an imperative for patients to make higher-value fulfillment decisions. AI has the potential to better guide these decisions by infusing individual cost and therapeutic efficacy data into suggested actions. This transparency can help care teams and patients work more collaboratively on medication management, adherence and dosage titration.

Though clinical care AI startups overall have been relatively slower to scale, the category continues to attract significant capital year-over-year, given its enormous potential and scarcity value of enterprise-grade products. Our belief is that this category will eventually sustain some of the most valuable startups in the health system segment.

Financial & Patient Engagement

The next highest funded categories have been financial or back-office AI startups as well as patient engagement AI startups. Patient engagement and revenue cycle management (RCM) workflows tend to be more repetitive, manual and less fraught with direct clinical risk. Here, AI applications can support significant double bottom line impact for health systems (i.e., revenue capture and labor efficiency). Importantly, the many jobs supporting these workflows consist of rote and deterministic activities, which means they can be more easily codified and automated. As a result, the functional areas in this category are popular targets for digital transformation.

Perhaps unsurprisingly, financial and back-office AI startups have seen some of the highest maturity rates, highest average valuations and, as we will assess in a future analysis, some of the most significant exits amongst all health system AI startups. In particular, middle and back-office RCM and patient scheduling startups have seen 11–20% maturity rates (2–4x greater than the health system AI average). Middle and back-office RCM products also have the highest average valuations across all health system functional areas. Given the higher success rate of companies operating in this category, as well as substantial untapped value creation potential, we expect that as AI evolves, health systems will double down on their efforts to continue to squeeze more value out of these areas.

The most successful products in this category leverage AI to capture and rationalize unstructured non-clinical and clinical data in support of billing decisions. The data captured or produced by AI is then used to create auditable and high-fidelity evidence of billable care that has a lower likelihood of being denied by a health plan. Given the sequential nature of revenue cycles, the most scaled startups also offer end-to-end solutions (front, middle and back-office RCM), where data and insights are collected longitudinally and models are trained on a more wholistic data set.

Patient benefit and billing AI startups, in particular, have seen an acceleration in both capital and valuation growth over the last 5 years — an interesting phenomenon suggesting this is a future opportunity area especially as patient financial responsibilities grow while collections rates tumble. Generative AI can be particularly useful in automating the high volume of patient communication activities that comprise this process.

Clinical Operations

Lastly, clinical operations and throughput is another evolving category that has not necessarily attracted as much capital as other categories, but has yielded amongst the highest maturity rates on capital invested, especially in the last 5 years. Startups operating in this category typically monitor inpatient utilization or clinical data and leverage AI to better predict where capacity constraints may emerge that risk delaying interventional procedures or bed utilization, both critical drivers of net patient services revenue for health systems. Some also optimize discharge or alternative site transfers. Nearly 18% of AI startups solving length of stay or patient throughput issues have reached maturity over the last 5 years, suggesting that, on average, these products are creating high relative value for their health system partners. Recent health system utilization data indicates that this is a value proposition of growing future importance.

Nonetheless, average valuations for these startups are lower than other functional areas, suggesting that while valuable, less relative budget may exist to support these initiatives and/or startups that focus exclusively on this category have lower revenue run rates or total addressable market than other areas. The most valuable startups in this category: (1) package their solutions as AI-enabled services, combining their technology with change management support and (2) have layered care coordination and management services into their modules, creating closed-loop tracking that increases value attributability through discharge or care transition.

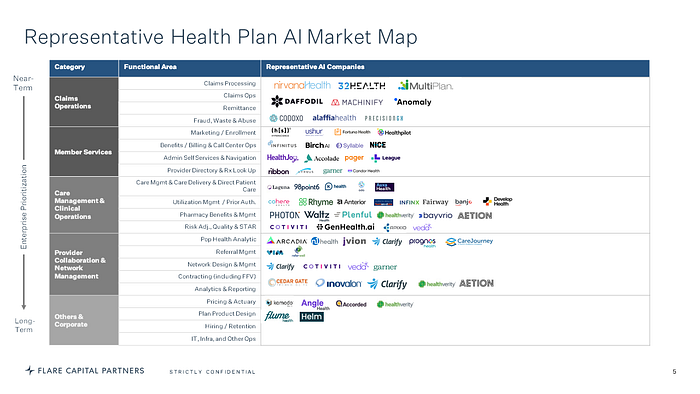

Health Plan AI Landscape: AI is Ushering in the Value-Based Care Evolution, though Plans Will Continue to Focus on streamlining the Member and Provider Experience of Care

Over the last decade, 119 AI startups selling primarily to health plans have raised $13.4 Billion in funding. This is a much smaller figure than the health system and life sciences segments, however, as we alluded to before, our dataset is limited to venture-backed startups, meaning the data may underrepresent the full magnitude of total AI spend among health plans. Considering that the largest insurer in the country, UnitedHealthcare, spends $5 Billion on data, technology, research and innovation annually, we believe that total spend on AI is likely higher and includes billions of dollars of investment into internal and non-venture backed technology efforts. That said, what stood out to us in this dataset is that financing and maturity were concentrated amongst a select few categories and functional areas.

Care Management

Almost $9.5 Billion of [PD2] health plan AI funding has been allocated to startups focused on care management and clinical operations, as shown below. This includes utilization management, risk adjustment and the many other foundational competencies required to support value-based contracting. Startups in this category have also been amongst the most enduring, with an average maturity rate (18%) that is nearly double the health plan AI average. Investing into value-based care capabilities has been arguably the largest shared priority of the last decade for health plans and risk-bearing entities. The complexity of the trilateral (patient, provider, plan) behavior change, care management evolution and novel data analytics required to succeed in value-based care, presents enormous opportunities for technology-enabled efficiency. Naturally, therefore, over 60 startups target this opportunity in a dedicated manner today, while countless others likely impact this opportunity indirectly. Additionally, the most successful startups in this area have built broad platforms supporting each of the priorities above.

A critical characteristic of the most successful startups in this category is their ability to bridge drop off points in a care workflow by pairing AI with humans, interchangeably. Startups in this category tend to have a unique ability to (1) tap into deeper, higher-utility training data sets to better anticipate population-level patient and provider behavioral tendencies, (2) use AI to extend clinical touch (i.e., calls, texts) at high friction or drop off points in an episode, collecting data while sustaining engagement, and (3) seamlessly fold gathered insights back into the care workflow to keep care teams more informed, with accretive impact to the care team’s experience of care. The net impact of this AI-enabled efficiency yields important outcomes like shorter times to care, more closed loop care, or completion of critical clinical activities (i.e., care gap closure, medication adherence) that impact medical loss ratios by driving lower cost utilization decisions. These gains are in addition to the labor productivity and cost efficiency AI can unlock to impact administrative loss ratios. Given the nascency of value-based care adoption, we expect this will continue to be a focus area for health plans over the near to medium term.

Member Services

Many of these same hallmarks are shared by AI startups that focus solely on member self-service, care navigation or administration, a category with a maturity rate that is 5x the health plan AI average. Startups in this area offer health plans and employers an ability to design member care experience programs that drive greater engagement in desired “high-value” activities, reducing medical spend. Almost all of these startups attribute this ability to proprietary AI models that allow them to relate to patient care preferences on a more personal level. Interestingly, maturity rates for companies supporting member services activities have increased in the couple of years, perhaps a microcosm of the surge in digital engagement brought about by the constraints of the pandemic.

Provider Collaboration and Network Management

Network management activities have also been a compelling target for AI-enabled automation. The backbone of a health plan’s ability to manage medical costs and therefore price their products competitively is the quality of their provider network. However, provider directory data tends to be frequently out-of-date, clinical outcomes are hard to attribute back to individual care providers and a lack of robust, customizable quality and outcomes metrics challenges the measurement of quality in a network. This is a good problem for AI, which can be used to comb and fill in directory data gaps (digitally and through automated outreach), as well as inform more actionable provider performance metrics by harmonizing clinical performance data that otherwise exists disparately in unstructured and semi-structured datasets.

Beyond just provider data, there is also a broader opportunity for AI to support better general data management, aggregation and cleansing (i.e., claims, contract, policy, clinical, social determinants, pharmacy) across the health plan enterprise. This would create a lot of downstream value for manual corporate processes like legal compliance and reporting.

Claims Operations

Notably, the claims operation category was amongst the lowest funded in this dataset, attracting $150 Million of funding according to our dataset. Like the health system RCM process, claims processing comprises a significant portion of health plan administrative overhead and is frequently targeted for automation efforts given its many deterministic workflows. The relatively lower funding rates captured in our dataset may reflect the fact that some insurers are developing homegrown solutions to address the opportunity. Others may be seeing sufficient yield by leveraging non-healthcare technology tools for this opportunity, which obviates additional spend on healthcare claims-focused AI startups. Despite lower funding levels, though, we believe that claims processing is a popular target of current and future AI-enabled automation efforts. Interestingly, over half of the funding in this category has been attracted to companies specializing in fraud, waste and abuse prevention, suggesting this is a higher yield target. This makes sense, given leading solutions in this functional area have proven they can use AI to rationalize coverage policies to billed claims, and unburden clinical and administrative teams from the research-based activities required to adjudicate a coverage decision.

Conclusion

We are still in the early innings of healthcare’s AI enabled transformation. Our analysis of funding data suggests that increased budgetary allocations to AI will be deployed with discretion, anchoring on functional areas where enterprise buyers can expand existing return on investment, like financial management, patient / member engagement and workflows that can extend human clinical touch.

In future analyses, we will explore opportunities across the life sciences enterprise and also benchmark financial and operating performance of different types of healthcare AI companies. In the meantime, please reach out with questions or comments (parth@flarecapital.com, jrubin@mba2024.hbs.edu). We welcome your thoughts!

Methodology and Disclaimers

Using Pitchbook data, we pulled a list of nearly 4,500 deals for companies that had raised venture capital funding from the beginning of 2014 through the end of 2023 (i.e., 10 calendar years-worth of deals). All companies included were headquartered in the United States, and were tagged in Pitchbook as Artificial Intelligence & Machine Learning companies in the Healthcare industry. We then manually reviewed this dataset to exclude deals 1) non-conformant with our definition of healthcare AI listed in footnote number 1 2) missing funding amounts 3) missing deal dates 4) selling to non-healthcare customers 5) reflecting post exit (IPO, M&A) or indeterminate financing rounds. We then manually created 50 unique sub-categorical tags for the health system, health plan and life sciences enterprise, and subjectively tagged each deal to one or more categories based on publicly available information (or our firsthand knowledge) of the startup’s most notable commercially viable product applications.

As a result, the data in this dataset is not mutually exclusive and all commercial applications may not be exhaustively captured by this dataset. Furthermore, the dataset is limited to data captured by Pitchbook as of January 1, 2024 and may not reflect every healthcare and digital health AI deal including participation by a venture capital fund.

Footnotes

- In our dataset, Healthcare AI is defined as any company selling exclusively to health systems, health plans or life sciences enterprises and offering either software products powered by AI or a service that distinctly leverages AI to optimize key components of its operating model; see Methodology for more details.

- Pitchbook Data

- US Census Business Trends and Outlooks, AI Supplement: https://www.census.gov/hfp/btos/data